General Communication, Inc.

2550 Denali Street, Suite 1000

Anchorage, Alaska 99503

(907) 868-5600

January 8, 2014

VIA EDGAR

Mr. Larry Spirgel, Assistant Director

United States Securities and Exchange Commission

Division of Corporation Finance

Washington, D.C. 20549

RE: General Communication, Inc.

Form 10-K for the Year Ended December 31, 2012

Filed March 8, 2013

Form 10-Q for Fiscal Quarter Ended September 30, 2013

Filed November 8, 2013

File No. 0-15279

Dear Mr. Spirgel:

This letter is provided in response to your letter dated December 24, 2013. Included below are your questions and comments, numbered consistent with your letter, with our answers immediately following each sequentially numbered item.

All comments will be addressed in future filings, as may be applicable based on the information provided below.

Form 10-Q for the quarterly period ended September 30, 2013

Condensed Notes to the Interim Consolidated Financial Statements

(1) Business and Summary of Significant Accounting Principles

(d) Acquisition, page 10

| |

1. | We note that the consideration ACS received includes entitlements to preferential cash distributions that are contingent on the future cash flows of AWN. Tell us how you evaluated this entitlement in assessing whether this is contingent consideration that would be included in the calculation of the purchase price. |

Response

Combining Wireless Networks. On June 4, 2012, we entered into an agreement (the “Contribution Agreement”) with ACS to create AWN, through certain of our respective subsidiaries, who would contribute substantially all the assets used in the respective wireless businesses (other than their respective retail wireless businesses) and certain related telecommunications transport assets. The transaction was publicly announced by us and a current report on Form 8-K describing the transaction was filed with the SEC on June 6, 2012. We entered into the transaction in order to:

| |

1. | Compete more effectively with the national carriers that had entered Alaska: AT&T and Verizon; |

| |

2. | Offer 4G LTE wireless services more rapidly and efficiently than each party otherwise could offer on its own due to spectrum and device compatibly issues; and |

| |

3. | Offer wider and lower-cost wireless coverage within Alaska. |

The Transaction. Under the terms of the Contribution Agreement, on July 22, 2013, ACS sold certain wireless assets to us for a cash payment of $100 million. ACS then contributed its remaining wireless assets to AWN for a one-third ownership interest and entitlements to receive preferential cash distributions totaling up to $190

Securities and Exchange Commission

January 8, 2014

Page 2

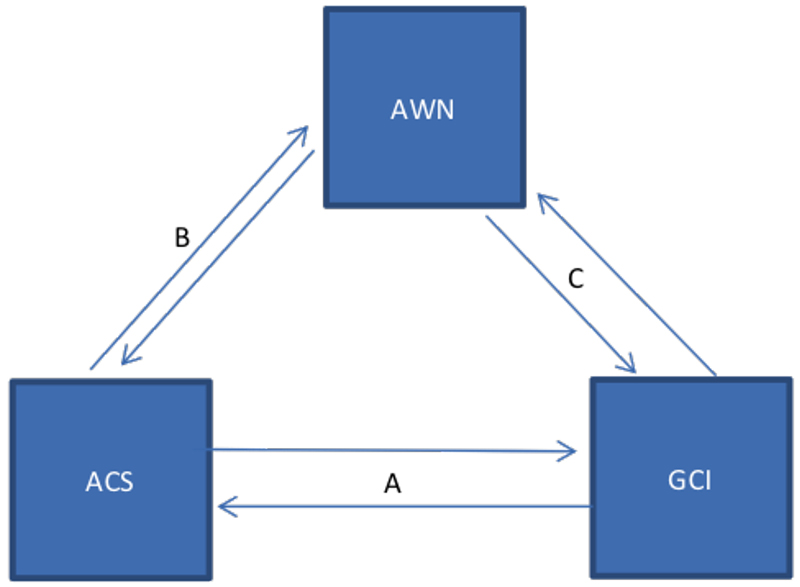

million (“Preference Payments”) contingent on AWN having sufficient future Adjusted Free Cash Flows and subject to certain possible subscriber adjustments described later in this section. These preferred distributions may exceed the distributions ACS would receive if it were entitled to one-third of the distributions made by AWN. After the preferred distributions are paid in full by mid-2017 or thereafter, ACS has a right to one-third of distributions and we have a right to two-thirds of distributions. The Preference Payments were negotiated between us and ACS to balance out the value of the respective parties’ wireless assets and risk and business objectives. We then contributed the purchased assets, together with our wireless assets, to AWN for a two-thirds controlling ownership interest in AWN and the right to residual distributions from AWN during the first four years (“Preference Period”). The assets sold or contributed included spectrum licenses, wireless switching and transmission equipment, cell sites, network usage rights, asset retirement obligations, leases, backhaul agreements, roaming agreements and other related assets. Pursuant to the terms of the transaction agreements, we are required to purchase wholesale wireless services from AWN for resale to their respective retail wireless customers. We will continue to compete with ACS for retail wireless customers. The transaction is further described in the diagram below.

| |

A. | ACS sold certain assets to GCI (purchased assets) for $100 million cash. |

| |

B. | ACS contributed its remaining wireless wholesale assets to AWN for a 1/3 ownership interest in AWN and rights to the preferred distributions. |

| |

C. | GCI contributed its wireless wholesale assets, including the purchased assets identified in “A” above, to AWN in exchange for a 2/3 ownership interest in AWN and the right to residual distributions from AWN during the Preference Period. |

AWN’s Sources of Revenue and Cost. AWN generates revenue from:

| |

(i) | Wholesale revenues it receives from ACS and GCI, which are anticipated to be approximately 70% of ACS’ |

and GCI’s retail wireless revenues;

| |

(ii) | Certain Federal telecommunication subsidies; |

| |

(iii) | Roaming revenues from other wireless carriers; and |

| |

(iv) | Revenues from providing data and voice backhaul services to other wireless carriers. |

Securities and Exchange Commission

January 8, 2014

Page 3

AWN is responsible for all operating and capital costs associated with operating, maintaining, and growing the wireless network, and will provide wireless equipment subsidies to ACS and GCI.

Distributions. On July 22, 2013, AWN, ACS and GCI (and/or certain of their affiliates) entered into the First Amended and Restated Operating Agreement of The Alaska Wireless Network, LLC (the “Operating Agreement”) and numerous other agreements. The Operating Agreement serves as AWN’s primary organizational document and contains detailed terms and conditions regarding the governance, operations and free cash flow distributions of AWN.

The Operating Agreement requires that all of AWN’s Adjusted Free Cash Flow be distributed to ACS and GCI. ACS is entitled to up to $190 million of preferred distributions from AWN’s Adjusted Free Cash Flow starting on July 23, 2013, with $50 million per year due in years one and two and $45 million per year due in years three and four. If AWN’s Adjusted Free Cash Flow is insufficient during the Preference Period to cover the distributions payable to ACS, the payment of preferred distributions may extend beyond the Preference Period. Although the preferred distributions to be made to ACS during the Preference Period are cumulative, the distributions have no preference in liquidation for any shortfalls in prior distributions or preferred distributions relating to future periods. We are entitled to distributions from AWN of all remaining Adjusted Free Cash Flow generated during the Preference Period. Effectively, we have the upside benefit and most of the downside risk of AWN’s Adjusted Free Cash Flow during the Preference Period. After the preferred distributions have been paid to ACS, distributions will be made to ACS and GCI in accordance with their respective ownership interests.

Both ACS’ and GCI’s distributions from AWN are subject to certain adjustments based on decreases in the number of ACS and GCI retail wireless connections, with a maximum aggregate adjustment of $21.8 million. ACS has four annual adjustment periods in 2015, 2016, 2017 and 2018 which are measured separately and both ACS and GCI have a cumulative adjustment in 2018. The possible wireless connection adjustments extend beyond the Preference Period. To the extent AWN distributions to ACS or GCI are inadequate to fund the connection adjustment (if any) in one period, the adjustment carries over to a future period. Unfunded connection adjustments have no preference in a liquidation of AWN.

The Operating Agreement has detailed definitions and explanations as to calculations of Adjusted Free Cash Flow, the wireless connection adjustments and the funding of distributions.

Accounting Treatment. We believe that the equity interest in AWN was issued to ACS as consideration in the business combination and would be subject to recognition and initial measurement based on Subtopic 805-30 but would be subject to classification based on guidance in ASC 480-10-15-10 which states “…when recognized, a financial instrument within the scope of this Topic that is issued as consideration (whether contingent or noncontingent) in a business combination shall be classified pursuant to the requirements of this Topic.” We evaluated the Preference Payment and concluded that it had two separate components - “Straight Preference Payments” that represent the preferred distribution excluding certain potential wireless connection adjustments and “Attrition Preference Payments” that represent the potential wireless connection adjustments. These two components were analyzed to determine if either component would be classified as a Freestanding Financial Instrument under ASC 480.

The ASC 480 glossary defines a Freestanding Financial Instrument as a financial instrument that meets either of the following conditions: “it is entered into separately and apart from any of the entity’s other financial instruments or equity transactions” or “it is entered into in conjunction with some other transaction and is legally detachable and separately exercisable.” We concluded that these provisions are embedded within the Operating Agreement and that they are not legally detachable from the equity interest leading us to determine that neither is a Freestanding Financial Instrument under ASC 480. We then determined that the equity interest is not mandatorily redeemable and thus, not within the scope of ASC 480, but would be classified as a noncontrolling interest by GCI.

We then considered the guidance in Subtopic 815-15 to determine whether a component of the Preference Payment is an embedded derivative that should be separated in accordance with ASC 815-15-25.

The host contract is the equity ownership granted to ACS that is governed by the Operating Agreement. We concluded that the Straight Preference Payments are clearly and closely related to the economic characteristics

Securities and Exchange Commission

January 8, 2014

Page 4

and risks of the Operating Agreement; therefore, they should not be bifurcated. We also noted that if the Straight Preference Payments were not considered clearly and closely related to the host contract, they would either not meet the definition of a derivative in ASC 815-10-15-83 or qualify for other exceptions including that in ASC 815-10-15-59d.

We concluded that the Attrition Preference Payments meet the three criteria for bifurcation, including the three characteristics in ASC 815-10-15-83. We then analyzed ASC 815 to determine whether a scope exception applied to its fact pattern. We concluded that the scope exception discussed within ASC 815-10-15-59b applied; therefore, we concluded that the Attrition Preference Payments should not be treated as a bifurcated embedded derivative.

Based on our analysis, we determined that the Preference Payment should be classified as a noncontrolling interest on our balance sheet.

Outline of the possible alternative answers considered and rejected.

Alternative No. 1: Account for the fair value of the Preference Payment as a separate liability such as contingent consideration

This approach would result in accounting for distributions to ACS during the Preference Period as principal and interest payments with all earnings of AWN allocated to us until the Preference Payment is satisfied. We rejected this approach because the Preference Payment is embedded within a financial instrument issued to ACS which is subject to classification under ASC 480 and ACS has the preferential right to free cash flow during the Preference Period with the contingency relating only to AWN’s ability to generate free cash flow because the Preference Payment is fixed and cumulative. This approach would also view ACS’s equity interest as a forward starting instrument with no allocation of earnings of AWN to noncontrolling interest during the Preference Period and would not faithfully present the rights and obligations of ACS and GCI under the Operating Agreement.

Alternative No. 2: Account for the fair value of the excess of the Preference Payment over what would be distributed to ACS in respect of its one-third equity interest as Contingent Consideration

We rejected this approach because the excess amount is embedded in a financial instrument issued to ACS which is subject to classification under ASC 480 and the Preference Payment relates to $190 million during the Preference Period with the contingency relating only to AWN’s ability to generate free cash flow because the Preference Payment is fixed and cumulative. Additionally, recognizing only the excess amount would result in the value of the contingent interest decreasing if AWN experiences better results than expected during the Preference Period and increasing if AWN experiences worse results than expected during the Preference Period. We also believed this accounting would not faithfully present the rights and obligations of ACS and GCI under the Operating Agreement.

Conclusion. Based on our analysis, we believe the Preference Payments are embedded in an equity interest issued as consideration transferred to ACS in the business combination in accordance with ASC 805. Further, we believe that the Preference Payments are not considered freestanding financial instruments as that term is defined in ASC 480. Further, we believe that the preference payments should not be bifurcated from the host equity interest based on the guidance in ASC 815. We are presenting the equity instrument issued to ACS as a noncontrolling interest. Additionally, the Preference Payments and Attrition Preference Payments were considered when determining the inputs used for the valuation of AWN and in the valuation of ACS’ equity interest.

(7) Segments, page 22

| |

2. | You disclose that you refocused your business in 2013 and now have two reportable segments. We note that the wireline segment includes a range of services to various types of customers. Tell us how you applied the guidance in ASC 280 in identifying your operating segments. If you have aggregated operating segments, please disclose this and provide us with your analysis of the aggregation criteria in ASC 280-10-50-11 for the various products and services you provide. |

Securities and Exchange Commission

January 8, 2014

Page 5

Response

At the beginning of 2013, we refocused our business on wireless operations due to changes in the wireless competitive environment, the increased importance of wireless services to our customers and the expected close of The Alaska Wireless Network (“AWN”) transaction. AT&T Mobility has been a competitor in the Alaska market for several years and at the beginning of 2013 we expected Verizon Wireless to enter the Alaska market in 2013 (which did occur). The competitive pressures caused by having two national carriers in the Alaska marketplace caused us to reevaluate our business focus. Additionally, to strengthen our competitive position, we entered into an agreement with Alaska Communications Systems Group, Inc. under which each company agreed to contribute its respective wireless assets to form AWN. AWN was formed to provide a robust, statewide network with the spectrum mix, scale, advanced technology and cost structure necessary to compete with Verizon Wireless and AT&T Mobility in Alaska. As a result of these changes in our market environment, we decided to manage our business by its Wireless and Wireline operations.

As a result, in 2013 the Chief Operating Decision Maker (“CODM”) role transitioned to our CEO rather than being shared by the CEO and EVP/COO. The EVP/COO is now responsible for the Wireline operations and the EVP, Wireless is responsible for Wireless operations.

Therefore, we reorganized our company to make key capital investment decisions and to assess operating performance by (1) Wireless operations and (2) Wireline operations which includes the remaining products and services we offer. These changes caused a segment reporting change in 2013 resulting in two reportable segments called Wireless and Wireline. The investment in capital is one of the primary strategic decisions made by our company and the majority of our capital assets are used by multiple customer or product types. Therefore, we make capital investment decisions at the segment level.

The Wireline segment includes the results of operations for all non-wholesale wireless products and services. To allow us to analyze and understand the results of our Wireline segment, our CODM receives financial reports that are stratified into customer types - consumer, business services and managed broadband. Within these customer types we further stratify into products and services such as retail wireless, Internet, video, School Access, Rural Health, long distance, local services and managed services. We do not internally charge overhead expenses (e.g. IT, accounting, human resources), depreciation and amortization expense, interest income, interest expense and income tax expense to the customer types; therefore, we do not have discrete financial information at this level. We do not have managers over any of the product types. We do not maintain or allocate any balance sheet accounts by customer or product types other than a balance sheet for cable that is prepared on an annual basis to test our cable certificates for impairment. Additionally, our Wireline segment shares infrastructure and no allocation of capital is done to track the financial results of our infrastructure sharing.

When our CODM makes decisions on the allocation of our Wireline segment capital expenditure budget he primarily reviews the expected return on investment for the product(s) impacted by the capital improvement. The various products we offer may be used by many different customer types. Beginning in 2013, we started maintaining a separate Wireless capital expenditure budget.

The primary report regularly reviewed by our CODM is the Consolidated Forecast. The Consolidated Forecast is delivered to the CODM monthly and is the subject of discussion in monthly financial review meetings. This document includes the earnings before depreciation and amortization expense, net interest expense, income taxes, share-based compensation expense, accretion expense, income or loss attributable to non-controlling interest, non-cash right-to-use expense and non-cash contribution adjustment (“Adjusted EBITDA”) results of the Wireless and Wireline segments including the stratification discussed above.

Although we have two reportable segments, we decided to provide the users of our financial statements with additional information on our Wireline segment by including revenue, cost of goods sold (excluding depreciation and amortization) and an allocation of selling, general and administrative expenses by customer type in our financial press releases. The additional information is provided to make it easier for us to explain changes in our operating results. Despite the additional income statement information provided, the key capital investment and operating decisions of the company are made at the segment level.

Securities and Exchange Commission

January 8, 2014

Page 6

As decisions regarding resource allocation are made at the segment level, we have concluded that we have two operating segments that are the same as our reportable segments; therefore, we do not aggregate operating segments.

Based on our reorganization at the beginning of 2013 including the change in our CODM and information presented to the CODM, we concluded that it was appropriate to change our segments to Wireless and Wireline in 2013.

We acknowledge our responsibility for the adequacy and accuracy of the disclosure in our filings.

We acknowledge that staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filings.

We acknowledge that we may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

If after you have had a chance to review this letter and still have questions regarding our accounting treatment, we respectfully request a conference with the staff to discuss your concerns and how we may adequately address them.

Please contact the undersigned at (907) 868-6952 if you have additional questions or require more information.

Sincerely,

/s/ Peter J. Pounds

Peter J. Pounds

Senior Vice President,

Chief Financial Officer,

Secretary and Assistant Treasurer

General Communication, Inc.